Medicaid vs. Obamacare

Obamacare is more than just health insurance – it’s a federal law and is really just the nickname for the Affordable Care Act (ACA). Medicaid is a government-run program that also offers health insurance. The expansion of the Medicaid program is a cornerstone of the ACA, and both offer affordable insurance options for individuals and families. It’s easy to see why they can be conflated.

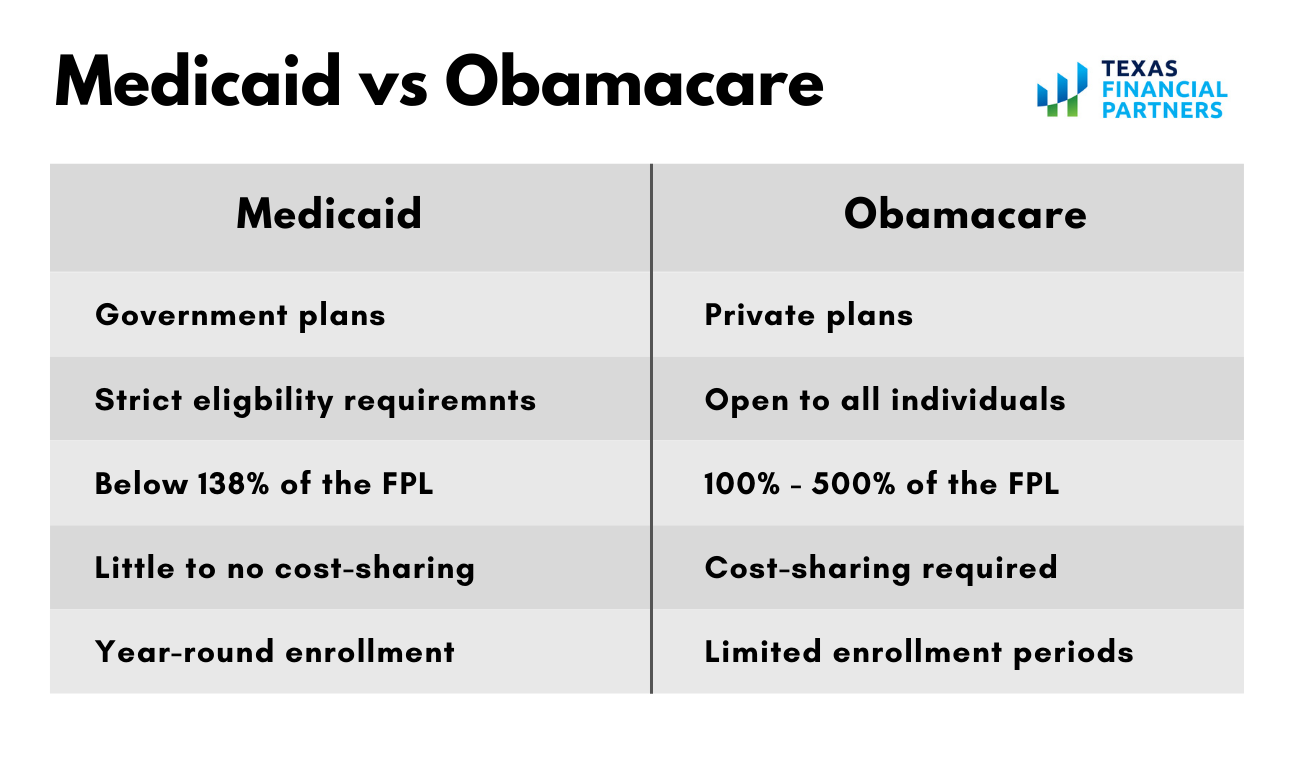

The biggest difference between the two is that Obamacare plans are offered by private insurance carriers, while Medicaid is a government program administered by each state. This article will discuss how Medicaid and Obamacare differ, including who is eligible for each, who provides coverage, enrollment periods, and how costs are shared.

Government vs. Private Plans

Let’s talk about how Medicaid and Obamacare are administered in a little more detail.

While Medicaid is a federal program, it is run by individual states who must follow federal guidelines. Some states followed proposals set forth by the Affordable Care Act and expanded their coverage, while others did not. Regardless, Medicaid is a social welfare program that provides health insurance to millions of U.S. citizens, including low-income adults, pregnant women, children, the elderly, and individuals with disabilities. It is funded at the state and federal government levels.

Obamacare plans are purchased through the Marketplace or Exchange, as some states call it. Private insurance companies offer Obamacare plans, which must comply with various federal and state regulations. Mainly, they must include the ten essential health benefits and cannot discriminate against individuals with pre-existing conditions.

Medicaid health plans are also offered by many private insurers, which is one reason why the two get confused. However, the private insurers who offer Medicaid plans have contracts with the state governments. Obamacare plans are not contracted with any form of government. Also, many states don’t call their Medicaid program by that name. They often use other names such as BadgerCare Plus in Wisconsin or Apple Health in the state of Washington.

Eligibility Guidelines

Eligibility for Medicaid is much more limited than it is for Obamacare.

To be eligible for Obamacare, you must be a legal U.S. citizen or resident, not be enrolled in Medicare, and not be incarcerated. As long as you meet those requirements, you can enroll in Obamacare, regardless of your income. If you hear someone say they aren’t eligible for Obamacare, it is likely that they mean they aren’t eligible for an Obamacare subsidy, which is dictated by income.

Obamacare subsidies and tax credits are based on household incomes. The total household income is measured against the federal poverty level (FPL) to determine if a person is eligible for a tax credit and, if so, how much. In 2022, individuals and families who have incomes that fall between 100% and 500% of the FPL qualify for subsidies. (The original guidelines only went up to 400% of the FPL, but it was extended in recent years due to COVID-19.)

A subsidy will lower your monthly premium for an Obamacare plan. They also offer cost-sharing reductions, which reduce out-of-pocket expenses if you’re enrolled in a Silver plan. Some states have additional subsidy options in addition to the federal ones outlined by the Affordable Care Act.

In most states, Medicaid is available for people who have an income of 138% or less of the FPL. In those states, the minimum FPL for an Obamacare subsidy is 139%. If your income is lower, you’ll be eligible for Medicaid. The exception to this is legal immigrants who have not met their five-year waiting period. If the person has not been a legal immigrant for at least five years, they can still qualify for an ACA subsidy if their income is less than 139% of the FPL.

Medicaid eligibility does vary somewhat from state to state. As we just mentioned, most states consider anything under 138% of the FPL to be Medicaid eligible. (A few states still have a lower requirement of 100% of the FPL.) States who abide by the 138% guideline provide free Medicaid coverage for adults under the age of 65.

If you live in a state that has not expanded Medicaid coverage, you must fall below the minimum income threshold and belong to at least one vulnerable group (disabled individuals, children, pregnant women, and elderly adults). So, if you are a non-disabled, 35-year-old male who has no children and earns $10,000 per year, you will not be eligible for Medicaid in those states.

Enrollment Periods

Obamacare has a specific open enrollment period. In most states, it’s from November 1 to December 15, with coverage beginning on January 1 of the upcoming year. Some states have extended the open enrollment in recent years, while others have opened it year-round for individuals who meet certain income requirements. You can also enroll in Obamacare during a special enrollment period if you qualify for one. Specific life events activate a special enrollment period – things like a loss of insurance, birth or adoption, or a change in marital status.

On the other hand, Medicaid enrollment is open year-round to all individuals who qualify. After you are accepted into the program, your coverage takes effect immediately, and there are no waiting periods. In addition, your Medicaid coverage could be retroactive. For example, a woman who applies for Medicaid while six months pregnant could retroactively get coverage for the first five months of prenatal care. Obamacare plans are never retroactive.

Cost-Sharing

If you are on Medicaid, most states do not require much (if any) cost-sharing by way of deductibles, coinsurance, or copayments.

Obamacare plans can have significant cost-sharing. The amount you’ll pay depends on which of the metal tiers you enroll in. In order of the most coverage, the levels are Premium, Gold, Silver, and Bronze. If your income is under 250% of the FPL and you enroll in a Silver plan, you are eligible for a cost-sharing reduction that would decrease those expenses.

The licensed insurance agents at Texas Financial Partners can help you apply for either Medicaid or an Obamacare plan, as well as other health insurance plans in Texas. If you want to learn more about which options are available to you, contact us today.